Table of Contents

By Moses Grader

The Municipality has not pushed for an operating override since its last successful operating override in 2005. Twenty years later, we are facing another consequential year. This year’s operating deficits are real because we have a perfect storm of revenue and cost shocks, coming after years of tightening.

A Brief History

The last two unsuccessful operating overrides in FY23 for $3.0M and in FY24 for $2.5M were majority driven by the District’s needs-based budgets from post-COVID staff increases. No overrides were sought for subsequent FY25 and FY26 budgets.

For the entire period of FY23 through FY26, the Municipal and District operating budgets were balanced through efficiency savings and cost cuts despite the headwinds of declining revenue growth and general inflationary pressures. The Municipality achieved savings by primarily: (i) improving overtime management, (ii) re-organizing certain functions to improve centralized resource management and (iii) realizing efficiencies from new technology in finance, audit and procurement. The District managed efficiencies by primarily (i) reducing staff levels through organic retirements, (ii) trimming balances in its revolver funds, (iii) streamlining other costs across the District.

From 2023 to 2026, the Municipal government full-time employee (FTE) headcount remained flat at 190; however, the Municipal FTE headcount has declined by nine people since 2018. From 2023 to 2026, the District staffing FTE headcount from the DESE database shows a decrease of 15, of which none were teacher FTEs, from 445 to 430; however, since 2018, FTE staffing headcount has decreased by 74 FTEs, of which 36 were teacher FTEs.

I think the FY26 Municipal budget of $48.0M is a reasonable baseline where the Municipality’s operations are running lean from a historical perspective. Similarly, the FY26 District Budget of $49.1M is also defensible in terms of dollar spend per student and the number of FTEs per student, both metrics are almost exactly at the average across all the DESE reporting districts in the Commonwealth. Despite 10-year declining enrollments of about 25% across the Commonwealth, most all Districts have increased their budgets in about the same proportion as the Marblehead schools.

Fiscal Year 2026 – A Look at Operational Cost Responsibility

To understand why we are suddenly in a big deficit situation this FY27, we can start by looking at the underlying numbers that made up the shared expenses of last year’s FY26 Municipal and District budget numbers.

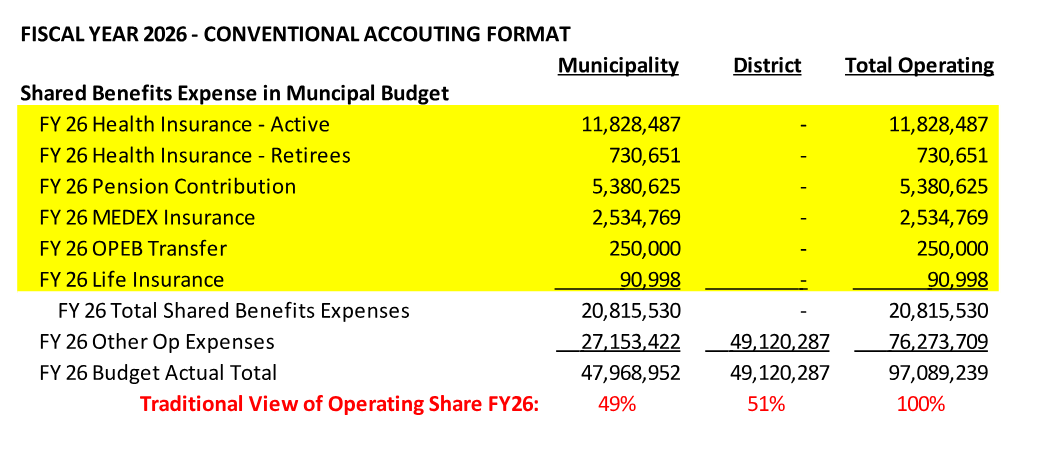

Most people do not realize that our conventional town accounting presentation for the Municipal side of the budget includes ALL benefits, mainly health care, pensions and MEDEX, for ALL employees of the town, including those employed by the District. The FY26 breakout of these benefits is shown below as part of the conventional Municipal budget presentation:

In FY26, total benefits costs amounted to approximately $20.8M, of which $8.6M was associated with Municipal employees and $12.2M was associated with District employees. If we reclassify the $12.2M District benefits expenses by adding them under the District budget of $49.1M, a more realistic picture of the District’s operational scope of responsibility in FY26 was a full $61.3M in budget expenditures. Similarly, the scope of the Municipal FY26 operating budget was closer to $35.8M, a much smaller number over which the Municipality actually had discretionary operational control. The following shows the reclassification of District costs to align with its operations:

Understanding the real scope of operating control over the town’s total $97.1M FY26 operating budget, 37% of which was controlled by the Municipality and 63% controlled by the District, helps us to appreciate how the Municipality’s smaller effective operating budget severely limits its capacity to absorb big operating cost swings in volatile years.

So, after reclassifying the $20.8M of shared benefits, the high-level side-by-side breakout was as follows for FY26:

Fiscal Year 2027 – The Perfect Storm

FY27 is a defining year largely due to the convergence of both revenue and cost shocks. As of this writing, the assumptions underlying the following analysis will likely change, but the framework should give clearer numeracy on the issues we are facing.

The first step is to identify how much new FY27 revenue is available to add to the FY26 budgets:

The above FY27 revenue share between the Municipality and the District is split on the basis of the "Aligned Operating Share" from the prior year FY26 budget. This FY27 is unusual because, instead of having increasing revenues to share, we expect a revenue decrease of approximately -$0.6M. The following shows the sources of that revenue deficit:

In addition to about $1.0M in declining local receipts, there is $2M less free cash than FY26 to fund operations in FY27.

The following table extends the FY27 analysis to show how the projected expenses for benefits are shared between the Municipality and the District and the extent to which their respective deficits need to be addressed by each to achieve a balanced overall budget in FY27:

In the above table, the FY27 "Discretionary Baseline after the Benefits" shows how much real discretionary operating budget is available for the Municipality and District after subtracting the appropriately allocated cost of benefits, as the biggest semi-discretionary cost driver at 20% of the overall operating budget. If the "Discretionary Level Services Budget Requests," which both Municipality and District develop early as part of their annual budgeting, exceed their respective "Discretionary Baseline After Benefits," then the deficits that arise can be tracked and shared appropriately between the Municipality and the District.

As of this writing, the Municipality and the District have assumed that they can trim approximately about $1.1M and $1.7M, respectively, which may not need to be restored in an override. However, even with these cost reductions, the Municipality will still need to cut an additional $3.3M in costs to meet its balanced budget responsibility and the Schools will need to cut an additional $1.5M in costs to meet its balanced budget responsibility for FY27 under this analysis.

Toward a FY27 restoration override request

With a total $4.8M deficit identified, the first-tier questions are: (i) what cuts need to be made to balance the budget and (ii) how are overrides or other funding mechanisms presented at Town Meeting to restore cuts or not. So far, the Select Board has deliberated on two funding scenarios to present the override questions, and I would also suggest we consider a third scenario:

- Deficit cuts of $4.8M restored with 100% override only

If the override does not pass, cuts would result in an initially estimated FTE reduction in the range of 50+ townwide. These are draconian cuts, which would likely have to be voted on at Town Meeting in a way that identifies each of the cuts, so that the Town understands what services will disappear next year if cuts are not restored by a vote.

- Deficit cuts of $4.8M restored with 60% override and 40% trash pickup fees

In this scenario, the Select Board, with the approval of the Board of Health, would seek to raise revenue with trash collection fees, which shifts about $2.0M off of the tax appropriation in FY27 onto fees appearing in resident utility bills. This would also be accompanied by override questions of about $2.8M to restore the remainder of the cuts to close the gap in the $4.8M total deficit. If the trash collection fees, which do not need a Town Meeting vote, were pushed through and the rest of the overrides did not pass, this would result in an initial estimated FTE reduction in the 30+ range townwide. If the trash collection fees were not approved and the override failed, then cuts are back to the levels of the first scenario above.

- Deficit cuts of $4.8M restored with 70% override and 30% from Stabilization Fund

This year may be a good year to deliberate on deploying the $1.5M available stabilization fund balance, which is subject to Town Meeting approval, to offset the free cash component of revenue declines. This would also be accompanied by an additional override request of about $3.3M to restore the remainder of the cuts to close the gap in the $4.8M total deficit. If the use of stabilization funds were approved but the override failed, this could result in an initial estimated FTE reduction in the 40 range townwide.

The above analysis and override scenarios are based on current assumptions of the currently available budget data and recent Select Board presentations.

Hard choices

This year is a critical year in which we have come in for a hard landing fiscally for the reasons enumerated here. Marbleheaders are generally tough but generous when it comes to funding their beloved Town. But they require clarity and trust in the democratic process by giving our legislative Town Meeting and voters a choice in the direction of the Town. Among comparable towns, we have earned our position for the lowest taxes as a share of both property value and residential income, a real achievement especially for our lower, middle- and fixed-income residents, although high housing prices and assessments driven by market demand still weigh heavily on the tax checkbooks of many residents. This year, Marbleheaders will make hard choices—and in so doing will also have the opportunity to better understand what goes into making our Town extraordinary.

Moses Grader is a Select Board member.

{kind=link}